Outline

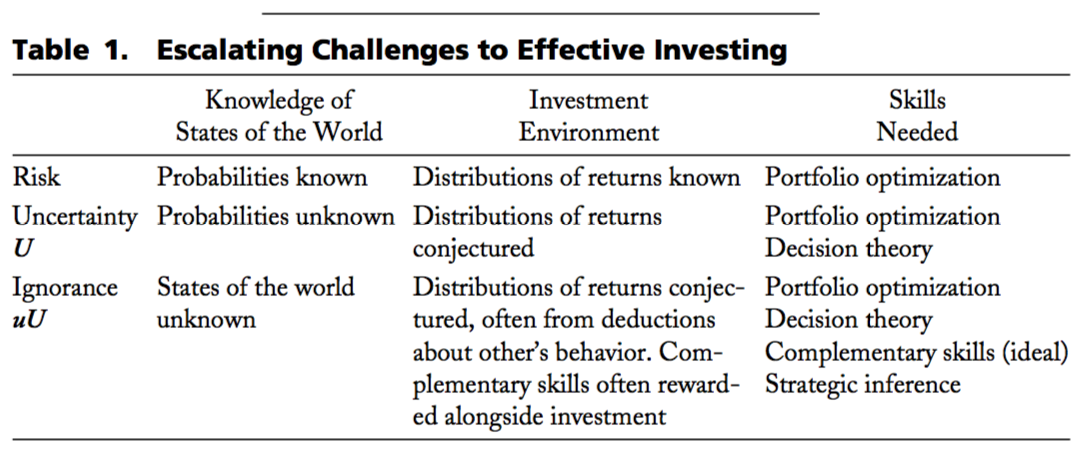

I. Risk Uncertainty and Ignorance

II. Behavioral Economics and Decision Traps

III. Math Whizzes in Finance and Cash Management

IV. Investing with Someone on the Other Side

V. Some Cautions: Herding, Cascades and Meltdowns

VI. A Buffett Tale

VII. Conclusion

Reading Notes

Putting it in context:

Professionals should read my article to see if they can identify situations in their own experience where the world was not merely uncertain but tended to the unknown and the unknowable. If the answer, as I expect, is yes, they should then take the lessons imparted here seriously and extend them with their own experience and insights.

But many unknowables are idiosyncratic or personal, affecting only individuals or handfuls of people, ... Such idiosyncratic uU situations, I argue below, present the greatest potential for significant excess investment returns.

But many unknowables are idiosyncratic or personal, affecting only individuals or handfuls of people, ... Such idiosyncratic uU situations, I argue below, present the greatest potential for significant excess investment returns.

Do not read on, however, if blame aversion is a prime concern: The world of uU is not for you. Consider this analogy. If in an unknowable world none of your bridges falls down, you are building them too strong. Similarly, if in an unknowable world none of your investments looks foolish after the fact, you are staying too far away from the unknowable. ... Just this peacemaking skill is required if one is to invest wisely in an unknowable world.

But it would be surprising not to see significant expected excess returns to investments that have three characteristics addressed in this essay:

(1) uU underlying features,

(2) complementary capabilities are required to undertake them, so the investments are not available to the general market, and

(3) it is unlikely that a party on the other side of the transaction is better informed. That is, uU may well work for you, if you can identify general characteristics of when such investments are desirable, and when not.

These very attractive three-pronged investments will not come along everyday. And when they do, they are unlikely to scale up as much as the investor would like, ...

Uniqueness. Many uU situations deserve a third U, for unique. ... An absence of competition from sophisticated and well-monied others spells the opportunity to buy underpriced securities.

Speculation 1: uUU investments—unknown, unknowable and unique—drive off speculators, which creates the potential for an attractive low price.

But since dozens of such situations have been seen over the years, speculators are willing to take positions in them. From the standpoint of investment, uniqueness is lost, just as the uniqueness of each child matters not to those who manufacture sneakers.

The standard model often does not apply to observations in the tails. ... That may be because the fundamental underlying factors produce thicker tails, or because there are rarely occurring anomalous or weird causes that produce extreme results, or both. The uU and uUU models would give great credence to the latter explanation, though both could apply.

A great percentage of uU investments, and a greater percentage of those that are uUU, provide great returns to a complementary skill.

For such efforts an ideal complementary skill is unusual judgment. Those who can sensibly determine when to plunge into and when to refrain from uUU investments gain a substantial edge, since mispricing is likely to be severe.

Miriam Avins, abandoned house to community garden story.

Few uU investment successes come from catching a secret.

Someone who knew Buffett and recognized his remarkable capabilities back then was in a privileged uU situation.

Maxim A : Individuals with complementary skills enjoy great positive excess returns from uU investments. Make a sidecar investment alongside them when given the opportunity.

competitive markets and arbitrage are not present in many uU situations, and in particular not the ones that interest us.

Speculation 2: Individuals who are overconfident of their knowledge will fall prey to poor investments in the uU world.

ambiguity aversion has the potential to exert a powerful effect. ... the more ambiguous the contingencies, the greater the aversion. If so, uU investments will drive away all but the most self-directed and rational thinking investors.

those who undertake prudent speculations in the unknown will be amply rewarded. Such speculations may include ventures into uncharted areas, where the finance professionals have yet to run their regressions, or may take completely new paths into already well-traveled regions (eg. the vanguard of computer assisted trading).

the more difficult a field is to investigate, the greater will be the unknowns and unknowables associated with it, and the greater the expected profits to those who deal sensibly with them.

Kelly Criterion, though mathematically correct, does not tell us how much to invest when one has an edge, since it ignores the structure of preferences.

(1) Most uU invest- ments are illiquid for a significant period, often of unknown length.

(2) Markets charge enormous premiums to cash out illiquid assets.

(3) Models of optimal sequential investment strategies tend to assume away the most important real-world challenges to such strategies, such as uncertain lock-in periods.

(4) There are substantial disagreements in the literature even about “toy problems,” such as those with immediate resolution of known-probability investments. The overall conclusion is that:

(5) Money management is a chal- lenging task in uU problems. e.g. margin calls.

That firm earns substantial excess returns through its combination of effective evaluation of uU situations, the ability to structure complex financial transactions, and the unusual complementary skill of being able to deal effectively with a great range of general partners.

people, even people in decision analysis and finance classrooms, where these experiments have been run many times, are very poor at taking account of the decisions of people on the other side of the table. ... (people are naturally very poor at drawing inferences from the fact that there is a willing seller on the other side of the market.)

individuals tend to extrapolate heuristics from situations where they make sense to those where they do not.

we are deeply inclined to trust our own information more than that of a counterpart, and are not well trained to know when this makes good sense, and when it inclines us to be a sucker.

(In uUU hard for everyone situation), First, only rarely will his information put you at severe disadvantage. Second, it is extremely unlikely that your counterpart is playing anything close to an optimal strategy.

(In a typical FX transaction,) there is no absolute advantage in such a situation, only informa- tion asymmetries.

Maxim B: When information asymmetries may lead your counterpart to be concerned about trading with you, identify for her important areas where you have an absolute advantage from trading. You can also identify her absolute advantages, but she is more likely to know those already. (does not apply to stocks.)

buyer, beware; seller-identified absolute advantages can be chimerical. Most swindles operate because the swindled one thinks he is in the process of getting a steal deal from someone else.

In the financial world at least, a key consideration in dealing with uU situations is assessing what others are likely to know or not know. ... Presumably Ricardo was not a military expert, but just understood that bidders would be few and that the market would over discount the uU risk.

The key to successfully dealing with situations where you find probabilities hard to estimate is to be able to assess whether others might be finding it easy. Be sensitive to telling signs that the other side knows more, (such as a smart person offering too favorable odds.)

Maxim C: In a situation where probabilities may be hard for either side to assess, it may be sufficient to assess your knowledge relative to the party on the other side (perhaps the market).

Maxim C: In a situation where probabilities may be hard for either side to assess, it may be sufficient to assess your knowledge relative to the party on the other side (perhaps the market).

An investor who could suffer significantly from any of these critiques might well be deterred from investing.

An investor who could suffer significantly from any of these critiques might well be deterred from investing.

Speculation 3: uU situations offer great investment potential given the combination of information asymmetries and lack of competition.

A key problem is to determine when you might be played for a sucker.

Given that, where betrayal is a risk, potential payoffs will be too high relative to what rational decision analysis would prescribe.

Gamblers opine that if you do not know who the sucker is in a game that you are the sucker. That does not automatically apply with uU investments. First, the other side may also be uninformed. Second, you may have a complementary skill, such as strong relations with Walmart, that may give you a significant absolute advantage multiple.

Maxim D: A significant absolute advantage offers some protection against potential selection. You should invest in a uU world if your advantage multiple is great, unless the probability is high the other side is informed and if, in addition, the expected selection factor is severe.

Still, many favorable deals will not get done, because the less informed party can not assess what it does not know. Both sides lose ex ante when there will be asymmetry on common value information, or when, as in virtually all uU situations, asymmetry is suspected.

(Citigroup) it is probably confident that other bidders were no better informed, and that both the bank and the Chinese government (which must approve the deal) may also not know the value of the bank, and were eager to secure foreign control. Great value may come from buying a pig in a poke, if others also can not open the bag.

In reality, the managers’ incentives are already enormous. Typical VC arrangements given bad outcomes cause serious ill will, and distort incentives—for example, they reward gambling behavior by managers after a bleak streak.

Maxim E: In uU situations, even sophisticated investors tend to underweight how strongly the value of assets varies. The goal should be to get good payoffs when the value of assets is high.

(In the oil well deal,) Davis would be happy to take his interest and give him the free override, thus reinforcing the message of the uninformative letter not placed on letter- head. ... Davis tried to play up the uU aspect of the situation to discourage participation.

Investors cluster as well. That may help them fend off criticism, but it will not protect them from meltdowns in value, be they for individual assets or for the market as a whole. There are two main ingredients in such meltdowns, information cascades and fat-tailed distributions.

The danger with an information cascade is that it is very difficult for the players to know how much information is possessed in total. When the total possessed is much less than the total assessed, prices can be well out of line.

(In housing bubble,) they did not contemplate that current house prices were based on little reliable information, and that big price movements, down as well as up, were quite possible.

If prices do not go up by 8%, the price will not merely soften; it will collapse, since rapid appreciation (not value to rent) was the basis for its high price. ... In (MidWest housing), there was much more information in the system.

In each case there was a dramatic run up before the big run down.

Maxim F: When there may be herding on information, beware. Be doubly beware if the information comes from extrapolating a successful past to a successful future.

(Buyers of mortgage backed securities,) they went with the herd to get a little extra kick by buying mortgage-backed securities. (for their own bonuses).

“Go to the Source,” namely engage in the “relentless pursuit of information from the field.”

Maxim G: Be triply beware of herding when there is evidence that there have been significant changes in the basic structure of markets, however stable they have been in the past.

That dramatically reduced the incentives for the banks that wrote them to scrutinize their safety. It also meant that no one really understood the risk characteristics of any package. ... mortgages had come to be written with extraordinarily low down payments.

past performance is not necessarily indicative of future results. Maxim G would tell us that past performance is particularly unreliable if basic assumptions from the past have been overturned.

A single year with 100 firms is closer to 1 observation than 100 independent observations.

(Buffett on 1987 Black Monday,) it was the computers that should have been jumping out of windows. Buffett was basically saying to Wall Street firms: “Even if you hire 100 brilliant Ph.D.s to run your models, no sensible estimate will emerge.” These are precisely the types of uU situations where the competition will be thin, the odds likely favorable, and the Buffetts of this world can thrive.

Maxim H: Discounting for ambiguity is a natural tendency that should be overcome, just as should be overeating.

Maxim I: Do not engage in the heuristic reasoning that just because you do not know the risk, others do. Think carefully, and assess whether they are likely to know more than you. When the odds are extremely favorable, sometimes it pays to gamble on the unknown, even though there is some chance that people on the other side may know more than you.

Putting money with the Gates Foundation represents sidecar philanthropy.

Learning to invest more wisely in a uU world may be the most promising way both to protect yourself from major investment errors, and to significantly bolster your prosperity.